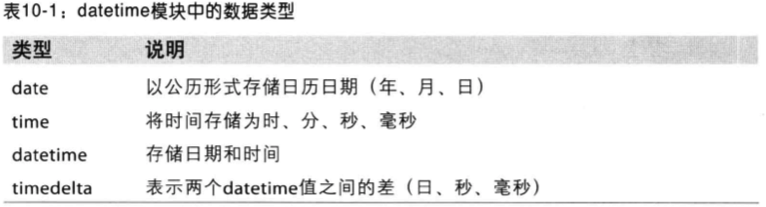

时间序列数据是一种重要的结构化数据形式。一般有几种:

- 时间戳:timestamp,特定的时刻

- 固定时期:period,如2010年全年

- 时间间隔:interval,有起始和结束时间戳表示;

- 实验或过程时间,每个时间点都是相对于特定时间的一个变量。

pandas提供一组标准时间序列处理工具和数据算法。

1. 日期和时间数据类型及工具

datetime模块:

In [1]: from datetime import datetime

In [2]: now = datetime.now()

In [3]: now

Out[3]: datetime.datetime(2017, 2, 17, 21, 11, 17, 866138)

In [4]: now.year,now.month,now.day

Out[4]: (2017, 2, 17)

时间差:timedelta

In [5]: delta = datetime(2011,1,7) - datetime(2008,6,24,7,14)

In [6]: delta

Out[6]: datetime.timedelta(926, 60360)

In [7]: delta.days

Out[7]: 926

In [8]: delta.seconds

Out[8]: 60360

In [9]: from datetime import timedelta

In [10]: start = datetime(2008,1,6)

In [11]: start + timedelta(12) # 传入days

Out[11]: datetime.datetime(2008, 1, 18, 0, 0)

In [12]: start - 2* timedelta(12)

Out[12]: datetime.datetime(2007, 12, 13, 0, 0)

datetime模块数据类型:

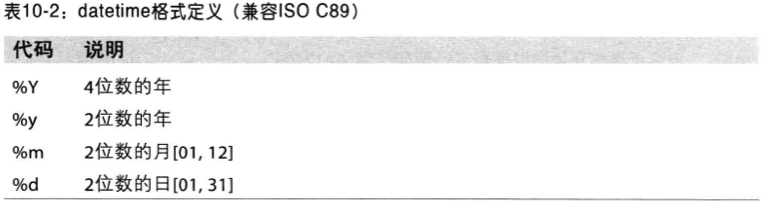

1.1 字符串和datetime的相互转换

In [13]: stamp = datetime(2011,1,3)

In [14]: str(stamp) # 转换为字符串

Out[14]: '2011-01-03 00:00:00'

In [15]: stamp.strftime('%Y-%m-%d') # 格式化为字符串

Out[15]: '2011-01-03'

# 可以转换我们日常用的格式

In [20]: from dateutil.parser import parse

In [21]: parse('2017-01-03')

Out[21]: datetime.datetime(2017, 1, 3, 0, 0)

In [22]: parse('Jan 31, 2017 10:23 PM')

Out[22]: datetime.datetime(2017, 1, 31, 22, 23)

In [23]: parse('02/11/2017')

Out[23]: datetime.datetime(2017, 2, 11, 0, 0)

# pandas模块的时间转换模块

In [25]: datestrs = ['7/6/2014','2/4/2016']

In [26]: import pandas as pd

In [27]: pd.to_datetime(datestrs)

Out[27]: DatetimeIndex(['2014-07-06', '2016-02-04'], dtype='datetime64[ns]', freq=None)

In [28]: idx = pd.to_datetime(datestrs + [None])

In [29]: idx

Out[29]: DatetimeIndex(['2014-07-06', '2016-02-04', 'NaT'], dtype='datetime64[ns]', freq=None)

In [30]: idx[2]

Out[30]: NaT

In [31]: pd.isnull(idx)

Out[31]: array([False, False, True], dtype=bool)

2. 时间序列基础

In [7]: dates = [(2011,1,1),(2011,2,3),(2011,2,4),(2011,4,23),(2011,4,22),(2011,

...: 4,1)]

In [8]: dates = [datetime(*x) for x in dates]

In [14]: ts = Series(np.random.randn(6), index=dates)

# 创建一个以时间戳为index的Series。

In [15]: ts

Out[15]:

2011-01-01 3.627969

2011-02-03 0.731217

2011-02-04 1.178071

2011-04-23 -2.085412

2011-04-22 -0.093829

2011-04-01 -0.157532

dtype: float64

In [16]: type(ts)

Out[16]: pandas.core.series.Series

In [17]: ts.index

Out[17]:

DatetimeIndex(['2011-01-01', '2011-02-03', '2011-02-04', '2011-04-23',

'2011-04-22', '2011-04-01'],

dtype='datetime64[ns]', freq=None)

# 和普通的Series一样,可以做Series相加

In [19]: ts + ts[::2]

2011-01-01 7.255939

2011-02-03 NaN

2011-02-04 2.356142

2011-04-01 NaN

2011-04-22 -0.187658

2011-04-23 NaN

dtype: float64

# 时间序列的index类型为datetime64,单位是纳秒

In [20]: ts.index.dtype

Out[20]: dtype('<M8[ns]')

In [21]: stamp = ts.index[0]

In [22]: stamp

Out[22]: Timestamp('2011-01-01 00:00:00')

2.1 索引、选取和子集的构造

索引

# 可以使用datetime格式的索引

In [24]: stamp = ts.index[2]

In [25]: ts[stamp]

Out[25]: 1.1780707665960897

# 也可以使用常用日期格式的字符串类型作为索引。

In [27]: ts['01/01/2011']

Out[27]:

2011-01-01 3.627969

dtype: float64

In [28]: ts['20110101']

Out[28]:

2011-01-01 3.627969

dtype: float64

切片

# 通过日期来直接切片,但是只对Series有效。

# pd.date_range可以将创建时间序列

In [29]: longer_ts = Series(np.random.randn(1000), index=pd.date_range('1/1/2017

...: ',periods=1000))

In [30]: longer_ts[:5]

Out[30]:

2017-01-01 0.311815

2017-01-02 -0.424868

2017-01-03 0.198069

2017-01-04 1.011494

2017-01-05 -0.312494

Freq: D, dtype: float64

In [31]: longer_ts[-5:]

Out[31]:

2019-09-23 -0.637869

2019-09-24 0.721613

2019-09-25 -0.914481

2019-09-26 0.036966

2019-09-27 0.677846

Freq: D, dtype: float64

# 获取2017-2月的所有数据

In [32]: longer_ts['2017-2']

Out[32]:

2017-02-01 1.258390

2017-02-02 0.606618

2017-02-03 0.927122

2017-02-04 0.761009

...

2017-02-23 -1.039703

2017-02-24 0.478075

2017-02-25 -0.328411

2017-02-26 -1.019641

2017-02-27 0.186212

2017-02-28 -1.466734

Freq: D, dtype: float64

# 单日数据

In [33]: longer_ts['2017-2-3']

Out[33]: 0.92712152603736908

# 年数据

In [34]: longer_ts['2017'][:5]

Out[34]:

2017-01-01 0.311815

2017-01-02 -0.424868

2017-01-03 0.198069

2017-01-04 1.011494

2017-01-05 -0.312494

Freq: D, dtype: float64

也可以通过不存在的时间戳对Series进行切片。

2.带有重复索引的时间序列

In [35]: dates = pd.DatetimeIndex(['1/1/2000','1/2/2000','1/2/2000','1/2/2000','

...: 1/3/2000'])

In [36]: dup_ts = Series(np.arange(5), index=dates)

In [37]: dup_ts

Out[37]:

2000-01-01 0

2000-01-02 1

2000-01-02 2

2000-01-02 3

2000-01-03 4

dtype: int64

# 查看索引是否重复

In [40]: dup_ts.index.is_unique

Out[40]: False

In [41]: dup_ts['1/2/2000'] # 重复, 数组

Out[41]:

2000-01-02 1

2000-01-02 2

2000-01-02 3

dtype: int64

In [42]: dup_ts['1/3/2000'] # 不重复,标量

Out[42]: 4

In [43]: grouped = dup_ts.groupby(level=0)

In [44]: grouped.mean()

Out[44]:

2000-01-01 0

2000-01-02 2

2000-01-03 4

dtype: int64

In [45]: grouped.count()

Out[45]:

2000-01-01 1

2000-01-02 3

2000-01-03 1

dtype: int64

3. 日期的范围、频率及移动

pandas中的时间序列一般是不规则的,没有固定的频率。但是通常需要一某种频率对序列进行分析, 幸运的是pandas有一套工具,帮助我们解决这些问题。

resample

In [49]: dates = pd.DatetimeIndex(['2000-01-02','2000-01-05','2000-01-07','2000-

...: 01-08','2000-01-10','2000-01-12'])

In [50]: ts = Series(np.random.randn(6), index=dates)

In [51]: ts

Out[51]:

2000-01-02 0.124049

2000-01-05 -0.840846

2000-01-07 -0.051655

2000-01-08 -0.603824

2000-01-10 0.467815

2000-01-12 -0.201388

dtype: float64

In [52]: ts.resample('D')

Out[52]: /Users/yangfeilong/anaconda/lib/python2.7/site-packages/IPython/utils/dir2.py:65:

FutureWarning: .resample() is now a deferred operation

use .resample(...).mean() instead of .resample(...)

canary = getattr(obj, '_ipython_canary_method_should_not_exist_', None)

DatetimeIndexResampler [freq=<Day>, axis=0, closed=left, label=left,

convention=start, base=0]

In [53]: ts.resample('D').mean() # 填充空日期

Out[53]:

2000-01-02 0.124049

2000-01-03 NaN

2000-01-04 NaN

2000-01-05 -0.840846

2000-01-06 NaN

2000-01-07 -0.051655

2000-01-08 -0.603824

2000-01-09 NaN

2000-01-10 0.467815

2000-01-11 NaN

2000-01-12 -0.201388

Freq: D, dtype: float64

3.1 生成日期范围

pandas.date_range可以生成指定长度的日期范围。

In [54]: index = pd.date_range('4/1/2017','6/1/2017') # 生成一段时间的序列,默认00:00

In [55]: index

Out[55]:

DatetimeIndex(['2017-04-01', '2017-04-02', '2017-04-03', '2017-04-04',

'2017-04-05', '2017-04-06', '2017-04-07', '2017-04-08',

'2017-04-09', '2017-04-10', '2017-04-11', '2017-04-12',

'2017-04-13', '2017-04-14', '2017-04-15', '2017-04-16',

'2017-04-17', '2017-04-18', '2017-04-19', '2017-04-20',

'2017-04-21', '2017-04-22', '2017-04-23', '2017-04-24',

'2017-04-25', '2017-04-26', '2017-04-27', '2017-04-28',

'2017-04-29', '2017-04-30', '2017-05-01', '2017-05-02',

'2017-05-03', '2017-05-04', '2017-05-05', '2017-05-06',

'2017-05-07', '2017-05-08', '2017-05-09', '2017-05-10',

'2017-05-11', '2017-05-12', '2017-05-13', '2017-05-14',

'2017-05-15', '2017-05-16', '2017-05-17', '2017-05-18',

'2017-05-19', '2017-05-20', '2017-05-21', '2017-05-22',

'2017-05-23', '2017-05-24', '2017-05-25', '2017-05-26',

'2017-05-27', '2017-05-28', '2017-05-29', '2017-05-30',

'2017-05-31', '2017-06-01'],

dtype='datetime64[ns]', freq='D')

In [56]: pd.date_range(start='4/1/2017',periods=20) # 指定长度

Out[56]:

DatetimeIndex(['2017-04-01', '2017-04-02', '2017-04-03', '2017-04-04',

'2017-04-05', '2017-04-06', '2017-04-07', '2017-04-08',

'2017-04-09', '2017-04-10', '2017-04-11', '2017-04-12',

'2017-04-13', '2017-04-14', '2017-04-15', '2017-04-16',

'2017-04-17', '2017-04-18', '2017-04-19', '2017-04-20'],

dtype='datetime64[ns]', freq='D')

In [57]: pd.date_range(end='4/1/2017',periods=20) # 指定结束日期

Out[57]:

DatetimeIndex(['2017-03-13', '2017-03-14', '2017-03-15', '2017-03-16',

'2017-03-17', '2017-03-18', '2017-03-19', '2017-03-20',

'2017-03-21', '2017-03-22', '2017-03-23', '2017-03-24',

'2017-03-25', '2017-03-26', '2017-03-27', '2017-03-28',

'2017-03-29', '2017-03-30', '2017-03-31', '2017-04-01'],

dtype='datetime64[ns]', freq='D')

In [58]: pd.date_range('4/1/2017','6/1/2017',freq='BM') # 指定频率,为月末工作日

Out[58]: DatetimeIndex(['2017-04-28', '2017-05-31'], dtype='datetime64[ns]', freq='BM')

In [59]: pd.date_range('5/3/2017 12:34:12',periods=5) # 默认时分秒 不变

Out[59]:

DatetimeIndex(['2017-05-03 12:34:12', '2017-05-04 12:34:12',

'2017-05-05 12:34:12', '2017-05-06 12:34:12',

'2017-05-07 12:34:12'],

dtype='datetime64[ns]', freq='D')

In [60]: pd.date_range('5/3/2017 12:34:12',periods=5, normalize=True) # 可以改到0时

Out[60]:

DatetimeIndex(['2017-05-03', '2017-05-04', '2017-05-05', '2017-05-06',

'2017-05-07'],

dtype='datetime64[ns]', freq='D')

3.2 频率和日期偏移量

In [61]: # 可以显式的创建频率使用的日期偏离

In [62]: from pandas.tseries.offsets import Hour

In [63]: four_hours = Hour(4)

In [64]: four_hours

Out[64]: <4 * Hours>

In [65]: # 也可以直接使用4H之类的字符串直接指定

In [66]: pd.date_range('1/1/2017', '1/3/2017 22:25',freq='4H')

Out[66]:

DatetimeIndex(['2017-01-01 00:00:00', '2017-01-01 04:00:00',

'2017-01-01 08:00:00', '2017-01-01 12:00:00',

'2017-01-01 16:00:00', '2017-01-01 20:00:00',

'2017-01-02 00:00:00', '2017-01-02 04:00:00',

'2017-01-02 08:00:00', '2017-01-02 12:00:00',

'2017-01-02 16:00:00', '2017-01-02 20:00:00',

'2017-01-03 00:00:00', '2017-01-03 04:00:00',

'2017-01-03 08:00:00', '2017-01-03 12:00:00',

'2017-01-03 16:00:00', '2017-01-03 20:00:00'],

dtype='datetime64[ns]', freq='4H')

In [67]: pd.date_range('1/1/2017', '1/3/2017 22:25',freq=four_hours)

Out[67]:

DatetimeIndex(['2017-01-01 00:00:00', '2017-01-01 04:00:00',

'2017-01-01 08:00:00', '2017-01-01 12:00:00',

'2017-01-01 16:00:00', '2017-01-01 20:00:00',

'2017-01-02 00:00:00', '2017-01-02 04:00:00',

'2017-01-02 08:00:00', '2017-01-02 12:00:00',

'2017-01-02 16:00:00', '2017-01-02 20:00:00',

'2017-01-03 00:00:00', '2017-01-03 04:00:00',

'2017-01-03 08:00:00', '2017-01-03 12:00:00',

'2017-01-03 16:00:00', '2017-01-03 20:00:00'],

dtype='datetime64[ns]', freq='4H')

In [68]: from pandas.tseries.offsets import Hour,Minute

# 可以通过相加获得指定长度的时间偏移

In [69]: Hour(1) + Minute(30)

Out[69]: <90 * Minutes>

# 也可以用更简单的字符串

In [70]: pd.date_range('1/1/2017',periods=3, freq='1h30min')

Out[70]:

DatetimeIndex(['2017-01-01 00:00:00', '2017-01-01 01:30:00',

'2017-01-01 03:00:00'],

dtype='datetime64[ns]', freq='90T')

有些偏移是不规律的,pandas自带了一些日期偏移量,供大家使用。如下表:

3.3 移动(超前或滞后)数据

shift沿着时间轴将数据进行前移或后移。

In [71]: ts = Series(np.random.randn(4), index=pd.date_range('1/1/2017',periods=

...: 4, freq='M'))

In [72]: ts

Out[72]:

2017-01-31 -0.080326

2017-02-28 0.432715

2017-03-31 1.094710

2017-04-30 -1.024227

Freq: M, dtype: float64

In [73]: ts.shift(2) # 将数据超前

Out[73]:

2017-01-31 NaN

2017-02-28 NaN

2017-03-31 -0.080326

2017-04-30 0.432715

Freq: M, dtype: float64

In [74]: ts.shift(-2) # 数据滞后

Out[74]:

2017-01-31 1.094710

2017-02-28 -1.024227

2017-03-31 NaN

2017-04-30 NaN

Freq: M, dtype: float64

# 计算本月相对上月的增长率

In [76]: ts/ts.shift(1) - 1

Out[76]:

2017-01-31 NaN

2017-02-28 -6.386994

2017-03-31 1.529866

2017-04-30 -1.935615

Freq: M, dtype: float64

# 加上freq后,日期增长,数据位置行不变

In [78]: ts.shift(2, freq='M')

Out[78]:

2017-03-31 -0.080326

2017-04-30 0.432715

2017-05-31 1.094710

2017-06-30 -1.024227

Freq: M, dtype: float64

# 当然还能加上其他频率,会更加灵活

In [79]: ts.shift(3, freq='D')

Out[79]:

2017-02-03 -0.080326

2017-03-03 0.432715

2017-04-03 1.094710

2017-05-03 -1.024227

dtype: float64

In [80]: ts.shift(1, freq='3D')

Out[80]:

2017-02-03 -0.080326

2017-03-03 0.432715

2017-04-03 1.094710

2017-05-03 -1.024227

dtype: float64

日期位移

# day:偏移日期,可传入数量

# MonthEnd:偏移到月末

In [81]: from pandas.tseries.offsets import Day,MonthEnd

In [82]: now = datetime(2017,2,18)

In [83]: now + 3 * Day() # 通过+-直接计算日期

Out[83]: Timestamp('2017-02-21 00:00:00')

In [84]: now + MonthEnd() # 偏移到月末

Out[84]: Timestamp('2017-02-28 00:00:00')

In [85]: now + MonthEnd(1) # 下月末

Out[85]: Timestamp('2017-02-28 00:00:00')

In [86]: offset = MonthEnd()

In [87]: offset.rollforward(now) # 滚到本月末

Out[87]: Timestamp('2017-02-28 00:00:00')

In [88]: offset.rollback(now) # 滚到上月末

Out[88]: Timestamp('2017-01-31 00:00:00')

In [90]: ts = Series(np.random.randn(20),index=pd.date_range('2/18/2017',periods

...: =20, freq='4d'))

In [91]: ts.groupby(offset.rollforward).mean() # 每个日期滚到月末后分组,并求平均值

Out[91]:

2017-02-28 -0.536243

2017-03-31 -0.373386

2017-04-30 0.131691

2017-05-31 1.775742

dtype: float64

In [92]: ts.resample('M',how='mean') # resample更易

/Users/yangfeilong/anaconda/bin/ipython:1: FutureWarning: how in .resample() is deprecated

the new syntax is .resample(...).mean()

#!/bin/bash /Users/yangfeilong/anaconda/bin/python.app

Out[92]:

2017-02-28 -0.536243

2017-03-31 -0.373386

2017-04-30 0.131691

2017-05-31 1.775742

Freq: M, dtype: float64

In [93]: ts.resample('M').mean()

Out[93]:

2017-02-28 -0.536243

2017-03-31 -0.373386

2017-04-30 0.131691

2017-05-31 1.775742

Freq: M, dtype: float64

4. 时区处理

时区处理很麻烦,一般就以UTC来处理。 UTC为协调世界时,是格林尼治时间的替代者,目前已经是国际标准。

In [1]: import pytz

In [4]: pytz.common_timezones[-5:]

Out[4]: ['US/Eastern', 'US/Hawaii', 'US/Mountain', 'US/Pacific', 'UTC']

In [5]: tz = pytz.timezone('Asia/Shanghai')

In [6]: tz

Out[6]: <DstTzInfo 'Asia/Shanghai' LMT+8:06:00 STD>

4.1 本地化和转换

默认情况下,pandas时间序列是单纯(naive)时区的。

In [11]: rng = pd.date_range('2/19/2017 9:30', periods=4, freq='D')

In [12]: ts = Series(np.random.randn(4),index=rng)

In [13]: ts.index.tz # 结果为空

In [14]: ts

Out[14]:

2017-02-19 09:30:00 0.530722

2017-02-20 09:30:00 1.459262

2017-02-21 09:30:00 -0.038216

2017-02-22 09:30:00 -0.671159

Freq: D, dtype: float64

# 可以在创建的时候直接赋值 tz=?

In [15]: pd.date_range('2/19/2017 9:30', periods=4, freq='D', tz='UTC')

Out[15]:

DatetimeIndex(['2017-02-19 09:30:00+00:00', '2017-02-20 09:30:00+00:00',

'2017-02-21 09:30:00+00:00', '2017-02-22 09:30:00+00:00'],

dtype='datetime64[ns, UTC]', freq='D')

# 从naive到有时区,使用tz_localize

In [16]: tz_utc = ts.tz_localize('UTC')

In [17]: tz_utc

Out[17]:

2017-02-19 09:30:00+00:00 0.530722

2017-02-20 09:30:00+00:00 1.459262

2017-02-21 09:30:00+00:00 -0.038216

2017-02-22 09:30:00+00:00 -0.671159

Freq: D, dtype: float64

In [18]: tz_utc.index.tz

Out[18]: <UTC>

# 使用 tz_convert进行修改时区

In [20]: tz_utc.tz_convert('Asia/Shanghai')

Out[20]:

2017-02-19 17:30:00+08:00 0.530722

2017-02-20 17:30:00+08:00 1.459262

2017-02-21 17:30:00+08:00 -0.038216

2017-02-22 17:30:00+08:00 -0.671159

Freq: D, dtype: float64

4.2 Timestamp对象

# 创建一个Timestamp对象

In [25]: stamp = pd.Timestamp('2017-2-19 12:10')

# naive to utc

In [26]: stamp_utc = stamp.tz_localize('UTC')

# 转换

In [29]: stamp_cn = stamp_utc.tz_convert('Asia/Shanghai')

# value 显示从unix纪元(1970.1.1)开始计算的纳秒数

In [30]: stamp_utc.value

Out[30]: 1487506200000000000

In [31]: stamp_cn.value

Out[31]: 1487506200000000000

In [32]: stamp.value # 三个都是一样的

Out[32]: 1487506200000000000

4.3 不同时区之间的运算

不同时区之间的运算最终都转换成了UTC,因为实际存储中都是以UTC时区来存储的。

In [33]: ts

Out[33]:

2017-02-19 09:30:00 0.530722

2017-02-20 09:30:00 1.459262

2017-02-21 09:30:00 -0.038216

2017-02-22 09:30:00 -0.671159

Freq: D, dtype: float64

In [34]: ts.index

Out[34]:

DatetimeIndex(['2017-02-19 09:30:00', '2017-02-20 09:30:00',

'2017-02-21 09:30:00', '2017-02-22 09:30:00'],

dtype='datetime64[ns]', freq='D')

In [35]: ts1 = ts[:2].tz_localize('Europe/London')

In [36]: ts2 = ts1.tz_convert('Europe/Moscow')

In [37]: result = ts1 + ts2 # ts1和ts2在不同的时区

In [38]: result.index # 结果都转变为了UTC

Out[38]: DatetimeIndex(['2017-02-19 09:30:00+00:00', '2017-02-20 09:30:00+00:00'], dtype='datetime64[ns, UTC]', freq='D')

In [39]: result

Out[39]:

2017-02-19 09:30:00+00:00 1.061445

2017-02-20 09:30:00+00:00 2.918524

Freq: D, dtype: float64

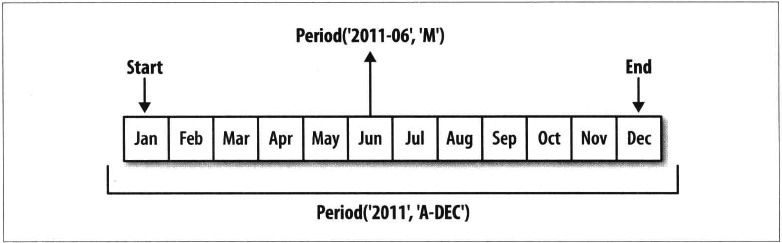

5. 时期及算术运算

period(时期)表示时间区间,如数日、数月等。

In [4]: p = pd.Period(2017)

In [5]: p

Out[5]: Period('2017', 'A-DEC')

In [6]: p + 1

Out[6]: Period('2018', 'A-DEC')

In [7]: pd.Period(2018) - p

Out[7]: 1

In [8]: rng = pd.period_range('1/1/2001','6/30/2001', freq='M')

In [9]: rng

Out[9]: PeriodIndex(['2001-01', '2001-02', '2001-03', '2001-04', '2001-05', '2001-06'], dtype='int64', freq='M')

In [10]: Series(np.random.randn(6), index=rng)

Out[10]:

2001-01 1.146489

2001-02 2.112800

2001-03 0.292746

2001-04 -0.841383

2001-05 -0.845565

2001-06 1.207504

Freq: M, dtype: float64

# 列表

In [11]: values = ['2001Q3','2002Q2','2003Q1']

In [13]: index = pd.PeriodIndex(values, freq='Q-DEC') # 以DEC月份作为年度最后一天,来计算季度

In [14]: index

Out[14]: PeriodIndex(['2001Q3', '2002Q2', '2003Q1'], dtype='int64', freq='Q-DEC')

In [26]: index.asfreq('Q-JUN') # 修改一下

Out[26]: PeriodIndex(['2002Q1', '2002Q4', '2003Q3'], dtype='int64', freq='Q-JUN')

5.1 period的频率转换

In [15]: p

Out[15]: Period('2017', 'A-DEC') # 按年取,取一年,年尾是12年31日

In [16]: p.asfreq('M', how='start') #

Out[16]: Period('2017-01', 'M')

In [17]: p.asfreq('M', how='end')

Out[17]: Period('2017-12', 'M')

In [18]: p = pd.Period('2017',freq='A-JUN') # 取2017年,以7月底为年终

In [19]: p.asfreq('M',how='end')

Out[19]: Period('2017-06', 'M')

In [20]: rng = pd.period_range('2006','2009',freq='A-DEC') # 取6-9的每年

In [21]: ts = Series(np.random.randn(len(rng)), index=rng)

In [22]: ts

Out[22]:

2006 -0.627032

2007 -1.409714

2008 0.072737

2009 1.240899

Freq: A-DEC, dtype: float64

In [23]: ts.asfreq('M', how='start') # 按月取,取第一个月

Out[23]:

2006-01 -0.627032

2007-01 -1.409714

2008-01 0.072737

2009-01 1.240899

Freq: M, dtype: float64

In [24]: ts.asfreq('B', how='end') # 修改频率到天,并取最后一天

Out[24]:

2006-12-29 -0.627032

2007-12-31 -1.409714

2008-12-31 0.072737

2009-12-31 1.240899

Freq: B, dtype: float64

5.2 按季度计算的时期频率

In [28]: rng = pd.period_range('2011Q3','2012Q4',freq='Q-JAN')

In [29]: rs = Series(np.arange(len(rng)), index=rng)

In [30]: new_rng = (rng.asfreq('B','e') - 1).asfreq('T','s') + 16*60

In [35]: rs.index = new_rng.to_timestamp()

In [36]: rs

Out[36]:

2010-10-28 16:00:00 0

2011-01-28 16:00:00 1

2011-04-28 16:00:00 2

2011-07-28 16:00:00 3

2011-10-28 16:00:00 4

2012-01-30 16:00:00 5

dtype: int64

5.3 将timestamp和period进行转换

In [38]: rng = pd.date_range('1/1/2001', periods=3, freq='M')

In [40]: ts = Series(np.random.randn(3), index=rng)

In [41]: pts = ts.to_period() # 转换成时期

In [42]: ts

Out[42]:

2001-01-31 0.619856

2001-02-28 -2.117066

2001-03-31 1.152329

Freq: M, dtype: float64

In [43]: pts

Out[43]:

2001-01 0.619856

2001-02 -2.117066

2001-03 1.152329

Freq: M, dtype: float64

In [45]: pts.to_timestamp(how='end') # 转换成时间戳

Out[45]:

2001-01-31 0.619856

2001-02-28 -2.117066

2001-03-31 1.152329

Freq: M, dtype: float64

5.4 通过数据创建PeriodIndex

In [47]: q = Series(range(1,5) * 7) # 创建季度

In [48]: y = Series(np.arange(1988,2016)) # 创建年份

In [49]: index = pd.PeriodIndex(year=y,quarter=q, freq='Q-DEC') # 创建index

In [50]: data = Series(np.random.randn(28), index=index)

In [51]: data

Out[51]:

1988Q1 -0.127187

1989Q2 -1.757196

1990Q3 0.826757

...

2013Q2 0.540955

2014Q3 0.531101

2015Q4 0.751739

Freq: Q-DEC, dtype: float64

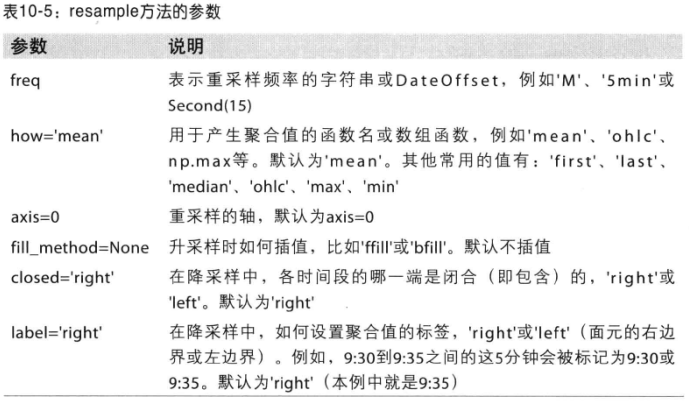

6. 重采样及频率转换

重采样(resample)表示将时间序列的频率进行转换的过程。可以分为降采样和升采样等。

pandas对象都有一个resample方法,可以进行频率转换。

In [5]: rng = pd.date_range('1/1/2000', periods=100, freq='D')

In [6]: ts = Series(np.random.randn(len(rng)), index=rng)

# 聚合后的值如何处理,使用mean(),默认即为mean,也可以使用sum,min等。

In [8]: ts.resample('M').mean()

Out[8]:

2000-01-31 -0.128802

2000-02-29 0.179255

2000-03-31 0.055778

2000-04-30 -0.736071

Freq: M, dtype: float64

In [9]: ts.resample('M', kind='period').mean()

Out[9]:

2000-01 -0.128802

2000-02 0.179255

2000-03 0.055778

2000-04 -0.736071

Freq: M, dtype: float64

6.1 降采样

# 12个每分钟 的采样

In [10]: rng = pd.date_range('1/1/2017', periods=12, freq='T')

In [11]: ts = Series(np.arange(12), index=rng)

In [12]: ts

Out[12]:

2017-01-01 00:00:00 0

2017-01-01 00:01:00 1

2017-01-01 00:02:00 2

...

2017-01-01 00:08:00 8

2017-01-01 00:09:00 9

2017-01-01 00:10:00 10

2017-01-01 00:11:00 11

Freq: T, dtype: int32

# 每隔五分钟采用,并将五分钟内的值求和,赋值到新的Series中。

# 默认 [0,4),前闭后开

In [14]: ts.resample('5min').sum()

Out[14]:

2017-01-01 00:00:00 10

2017-01-01 00:05:00 35

2017-01-01 00:10:00 21

Freq: 5T, dtype: int32

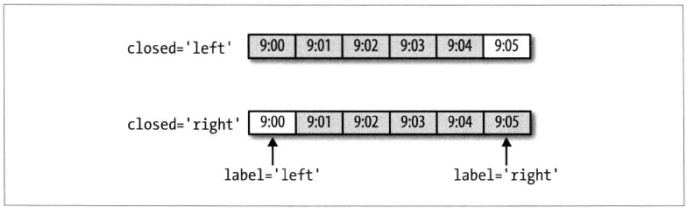

# 默认 closed就是left,

In [15]: ts.resample('5min', closed='left').sum()

Out[15]:

2017-01-01 00:00:00 10

2017-01-01 00:05:00 35

2017-01-01 00:10:00 21

Freq: 5T, dtype: int32

# 调整到右闭左开后,但是时间取值还是left

In [16]: ts.resample('5min', closed='right').sum()

Out[16]:

2016-12-31 23:55:00 0

2017-01-01 00:00:00 15

2017-01-01 00:05:00 40

2017-01-01 00:10:00 11

Freq: 5T, dtype: int32

# 时间取值也为left,默认

In [17]: ts.resample('5min', closed='left', label='left').sum()

Out[17]:

2017-01-01 00:00:00 10

2017-01-01 00:05:00 35

2017-01-01 00:10:00 21

Freq: 5T, dtype: int32

还可以调整offset

# 向前调整1秒

In [18]: ts.resample('5T', loffset='1s').sum()

Out[18]:

2017-01-01 00:00:01 10

2017-01-01 00:05:01 35

2017-01-01 00:10:01 21

Freq: 5T, dtype: int32

OHLC重采样

金融领域有一种ohlc重采样方式,即开盘、收盘、最大值和最小值。

In [19]: ts.resample('5min').ohlc()

Out[19]:

open high low close

2017-01-01 00:00:00 0 4 0 4

2017-01-01 00:05:00 5 9 5 9

2017-01-01 00:10:00 10 11 10 11

利用groupby进行重采样

In [20]: rng = pd.date_range('1/1/2017', periods=100, freq='D')

In [21]: ts = Series(np.arange(100), index=rng)

In [22]: ts.groupby(lambda x: x.month).mean()

Out[22]:

1 15.0

2 44.5

3 74.0

4 94.5

dtype: float64

In [23]: rng[0]

Out[23]: Timestamp('2017-01-01 00:00:00', offset='D')

In [24]: rng[0].month

Out[24]: 1

In [25]: ts.groupby(lambda x: x.weekday).mean()

Out[25]:

0 50.0

1 47.5

2 48.5

3 49.5

4 50.5

5 51.5

6 49.0

dtype: float64

6.2 升采样和插值

低频率到高频率的时候就会有缺失值,因此需要进行插值操作。

In [26]: frame = DataFrame(np.random.randn(2,4), index=pd.date_range('1/1/2017'

...: , periods=2, freq='W-WED'), columns=['Colorda','Texas','NewYork','Ohio

...: '])

In [27]: frame

Out[27]:

Colorda Texas NewYork Ohio

2017-01-04 1.666793 -0.478740 -0.544072 1.934226

2017-01-11 -0.407898 1.072648 1.079074 -2.922704

In [28]: df_daily = frame.resample('D')

In [30]: df_daily = frame.resample('D').mean()

In [31]: df_daily

Out[31]:

Colorda Texas NewYork Ohio

2017-01-04 1.666793 -0.478740 -0.544072 1.934226

2017-01-05 NaN NaN NaN NaN

2017-01-06 NaN NaN NaN NaN

2017-01-07 NaN NaN NaN NaN

2017-01-08 NaN NaN NaN NaN

2017-01-09 NaN NaN NaN NaN

2017-01-10 NaN NaN NaN NaN

2017-01-11 -0.407898 1.072648 1.079074 -2.922704

In [33]: frame.resample('D', fill_method='ffill')

C:\Users\yangfl\Anaconda3\Scripts\ipython-script.py:1: FutureWarning: fill_metho

d is deprecated to .resample()

the new syntax is .resample(...).ffill()

if __name__ == '__main__':

Out[33]:

Colorda Texas NewYork Ohio

2017-01-04 1.666793 -0.478740 -0.544072 1.934226

2017-01-05 1.666793 -0.478740 -0.544072 1.934226

2017-01-06 1.666793 -0.478740 -0.544072 1.934226

2017-01-07 1.666793 -0.478740 -0.544072 1.934226

2017-01-08 1.666793 -0.478740 -0.544072 1.934226

2017-01-09 1.666793 -0.478740 -0.544072 1.934226

2017-01-10 1.666793 -0.478740 -0.544072 1.934226

2017-01-11 -0.407898 1.072648 1.079074 -2.922704

In [34]: frame.resample('D', fill_method='ffill', limit=2)

C:\Users\yangfl\Anaconda3\Scripts\ipython-script.py:1: FutureWarning: fill_metho

d is deprecated to .resample()

the new syntax is .resample(...).ffill(limit=2)

if __name__ == '__main__':

Out[34]:

Colorda Texas NewYork Ohio

2017-01-04 1.666793 -0.478740 -0.544072 1.934226

2017-01-05 1.666793 -0.478740 -0.544072 1.934226

2017-01-06 1.666793 -0.478740 -0.544072 1.934226

2017-01-07 NaN NaN NaN NaN

2017-01-08 NaN NaN NaN NaN

2017-01-09 NaN NaN NaN NaN

2017-01-10 NaN NaN NaN NaN

2017-01-11 -0.407898 1.072648 1.079074 -2.922704

In [35]: frame.resample('W-THU', fill_method='ffill')

C:\Users\yangfl\Anaconda3\Scripts\ipython-script.py:1: FutureWarning: fill_metho

d is deprecated to .resample()

the new syntax is .resample(...).ffill()

if __name__ == '__main__':

Out[35]:

Colorda Texas NewYork Ohio

2017-01-05 1.666793 -0.478740 -0.544072 1.934226

2017-01-12 -0.407898 1.072648 1.079074 -2.922704

In [38]: frame.resample('W-THU').ffill()

Out[38]:

Colorda Texas NewYork Ohio

2017-01-05 1.666793 -0.478740 -0.544072 1.934226

2017-01-12 -0.407898 1.072648 1.079074 -2.922704

6.3 通过时期(period)进行重采样

# 创建一个每月随机数据,两年

In [41]: frame = DataFrame(np.random.randn(24,4), index=pd.date_range('1-2017',

...: '1-2019', freq='M'), columns=['Colorda','Texas','NewYork','Ohio'])

# 每年平均值进行重采样

In [42]: a_frame = frame.resample('A-DEC').mean()

In [43]: a_frame

Out[43]:

Colorda Texas NewYork Ohio

2017-12-31 -0.441948 -0.040711 0.036633 -0.328769

2018-12-31 -0.121778 0.181043 -0.004376 0.085500

# 按季度进行采用

In [45]: a_frame.resample('Q-DEC').ffill()

Out[45]:

Colorda Texas NewYork Ohio

2017-12-31 -0.441948 -0.040711 0.036633 -0.328769

2018-03-31 -0.441948 -0.040711 0.036633 -0.328769

2018-06-30 -0.441948 -0.040711 0.036633 -0.328769

2018-09-30 -0.441948 -0.040711 0.036633 -0.328769

2018-12-31 -0.121778 0.181043 -0.004376 0.085500

In [49]: frame.resample('Q-DEC').mean()

Out[49]:

Colorda Texas NewYork Ohio

2017-03-31 -0.445315 0.488191 -0.543567 -0.459284

2017-06-30 -0.157438 -0.680145 0.295301 -0.118013

2017-09-30 -0.151736 0.092512 0.684201 -0.035097

2017-12-31 -1.013302 -0.063404 -0.289404 -0.702681

2018-03-31 0.157538 -0.175134 -0.548305 0.609768

2018-06-30 -0.231697 -0.094108 0.224245 -0.151958

2018-09-30 -0.614219 0.308801 -0.205952 0.154302

2018-12-31 0.201266 0.684613 0.512506 -0.270111

7. 时间序列绘图

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

from pandas import Series,DataFrame

frame = DataFrame(np.random.randn(20,3),

index = pd.date_range('1/1/2017', periods=20, freq='M'),

columns=['randn1','randn2','randn3']

)

frame.plot()

8. 移动窗口函数

待续。。。

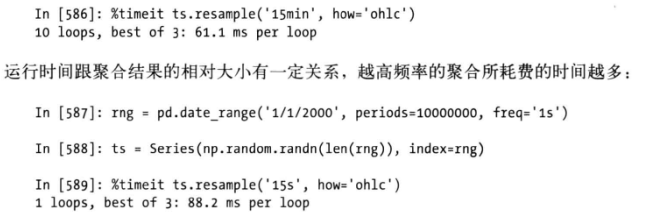

9. 性能和内存使用方面的注意事项

In [50]: rng = pd.date_range('1/1/2017', periods=10000000, freq='1s')

In [51]: ts = Series(np.random.randn(len(rng)), index=rng)

In [52]: %timeit ts.resample('15s').ohlc()

1 loop, best of 3: 222 ms per loop

In [53]: %timeit ts.resample('15min').ohlc()

10 loops, best of 3: 152 ms per loop

貌似现在还有所下降。